How to Start Filing for Bankruptcy in Florida With an Attorney

Bankruptcy

How to Start Filing for Bankruptcy in Florida With an Attorney

Filing for bankruptcy in Florida starts with one phone call to a licensed bankruptcy attorney. Your attorney will review your income, debts, and assets, help you pass the means test, and file your petition with the U.S. Bankruptcy Court.

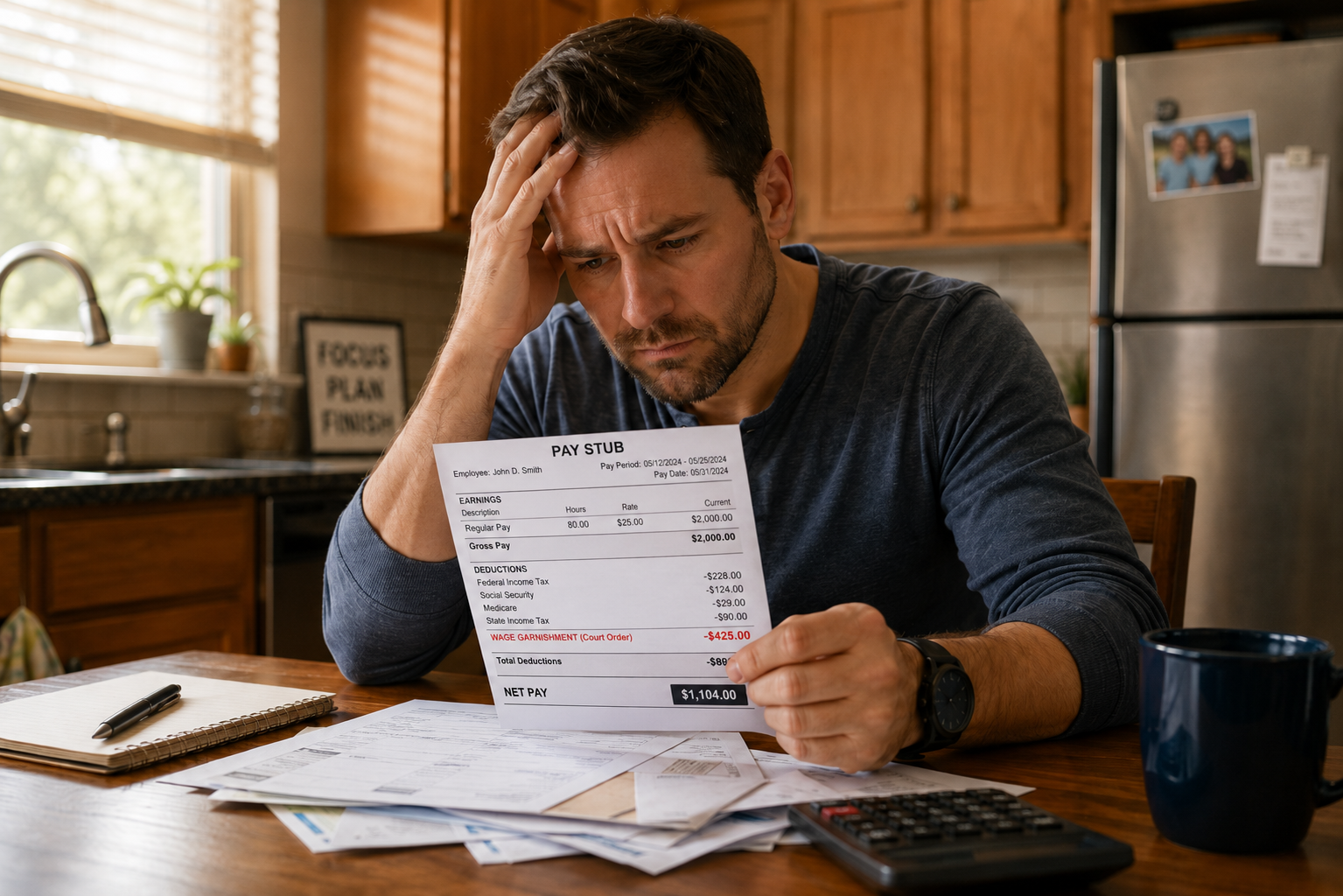

From that moment, an automatic stay goes into effect and creditors must stop collection activity immediately upon filing because of the automatic stay. If you are buried under credit card debt, facing wage garnishment, or getting sued by a lender, bankruptcy may be the legal fresh start you have been waiting for.

What Happens When You File for Bankruptcy in Florida

Most people put off filing because they do not know what to expect. Here is a plain-language walkthrough of the process from the first call to your discharge.

Step 1: Talk to a Florida Bankruptcy Attorney

Your first step is a confidential consultation. At Peck Law Firm, attorney Rick Peck and his team listen to your full financial picture before recommending any specific chapter.

During that first conversation, your attorney will want to know:

- Your income and expenses: This determines whether you qualify for Chapter 7 or whether Chapter 13 makes more sense.

- What you owe and to whom: Credit cards, medical bills, personal loans, mortgage arrears, and student loan balances all factor into the strategy.

- What assets you own: Your home, car, retirement accounts, and personal property will be evaluated against Florida's bankruptcy exemptions.

- Whether you are being sued or garnished: If a creditor has already filed suit or is garnishing your wages, timing your filing carefully can stop that harm fast.

You do not need to have everything organized before you call. Your attorney will guide you through what to gather.

Step 2: Gather Your Financial Documents

Once you decide to move forward, and after your initial consultation, your attorney's office will give you a document checklist. Gathering these materials promptly keeps your case on track.

You will typically need:

- Pay stubs: The last six months of income records are required for the Chapter 7 means test.

- Tax returns: Usually the last two years of federal returns.

- Bank statements: Recent statements for every account you hold.

- A complete debt list: Account numbers, balances, and creditor addresses for every debt you owe.

- Property valuations: A recent appraisal or market estimate for real estate, vehicle values through Kelley Blue Book, and a list of personal property.

- Mortgage or lease documents: Needed if you are behind on payments or want to keep your home or car through a reaffirmation agreement.

Your attorney may also ask for documentation of any pending lawsuits, garnishment orders, or collection letters. Bring everything you have.

Step 3: Pass the Means Test or Build Your Repayment Plan

This step is where your attorney earns their value.

For Chapter 7 bankruptcy: The bankruptcy means test compares your average monthly income over the last six months to the Florida median income for your household size. If your income is at or below the median, you generally qualify. If it is above the median, a more detailed expense calculation is applied. A Florida bankruptcy attorney knows how to work through that calculation accurately so you do not lose eligibility over a technical error.

For Chapter 13 bankruptcy: Instead of a means test, your attorney calculates your disposable income and builds a structured repayment plan lasting three to five years. This chapter is often the right choice if you are behind on a mortgage and want to stop foreclosure, if you have non-exempt assets you want to keep, or if your income is too high for Chapter 7.

For Chapter 11 bankruptcy: Typically used by businesses or individuals with very high debt levels, Chapter 11 allows for debt reorganization while you continue operating. It is more complex and your attorney will discuss whether it fits your situation.

The U.S. Bankruptcy Court for the Middle District of Florida handles cases filed in the Tampa, Orlando, Jacksonville, and Fort Myers divisions. Attorney Rick Peck is admitted to practice in that court, which means local familiarity matters for your case.

Step 4: Complete Required Credit Counseling

Before your petition can be filed, federal law requires you to complete a credit counseling course from an approved provider. This course takes about 90 minutes and can be done online or by phone. Your attorney's office will point you to a court-approved agency.

A second course, called debtor education, is required after your case is filed and before your discharge is granted. Your attorney will remind you when to complete it.

Step 5: File Your Petition and Trigger the Automatic Stay

Your attorney prepares and files your bankruptcy petition, schedules, and statements with the bankruptcy court. This is a detailed set of documents disclosing all of your income, debts, assets, and financial transactions from the past few years.

The moment the court receives your filing, the automatic stay goes into effect under 11 U.S.C. § 362. This federal protection immediately prohibits:

-

Creditor calls and letters: All collection contact must stop by law.

-

Wage garnishment: Most wage garnishments for consumer debts are suspended by the automatic stay, although certain obligations, such as domestic support obligations, are treated differently.

-

Foreclosure proceedings: Lenders cannot proceed with a foreclosure sale while your case is active.

-

Lawsuits and judgments: Pending credit card lawsuits are paused.

If a creditor violates the automatic stay after being notified of your filing, your attorney can seek sanctions against them in court.

Step 6: Attend the 341 Meeting of Creditors

Roughly 30 to 45 days after filing, you will attend a meeting of creditors, sometimes called the 341 meeting. This is not a courtroom hearing before a judge. It is a brief meeting with the bankruptcy trustee assigned to your case, typically lasting 10 to 15 minutes.

The trustee will ask you questions about your petition under oath to confirm the accuracy of your filings. Your attorney will be with you. Creditors are legally allowed to attend but rarely do, especially in consumer Chapter 7 cases.

Many clients ask whether they have to appear in person. In most Middle District of Florida cases today, 341 meetings are conducted by phone or video. Your attorney will confirm the format for your specific case.

Step 7: Receive Your Discharge

In a Chapter 7 case, your discharge typically comes 60 to 90 days after your 341 meeting if no objections are filed. The discharge is the court order that legally eliminates your obligation to pay the listed debts. Credit card balances, medical bills, and most personal loan balances are wiped out.

In a Chapter 13 case, your discharge comes after you complete your three-to-five-year repayment plan. At the end of the plan, remaining eligible balances are discharged.

After discharge, you are legally free from those debts. Creditors cannot attempt to collect them. This is the fresh start the law is designed to give you.

What You Can Keep When You File for Bankruptcy in Florida

One of the biggest fears people have about filing is losing their home, car, or retirement savings. Florida's bankruptcy exemption laws are actually among the most protective in the country.

Florida Homestead Exemption

Florida's homestead exemption can provide substantial protection for a primary residence. However, federal law may limit the amount of certain recently acquired homestead equity if the property was acquired within 1,215 days before filing. If you have not met that residency requirement, a federal cap applies. This means most Florida homeowners can protect their home equity entirely.

Vehicle Exemption

Florida allows you to exempt up to $5,000 in vehicle equity, or up to $9,000 if you are not claiming the homestead exemption on real property. For most people with a financed car, the equity is minimal and the vehicle is kept by reaffirming the loan with the lender.

Retirement Accounts

IRAs, 401(k)s, pensions, and most other retirement accounts are fully protected in Florida bankruptcy cases under both federal and state law. You do not lose your retirement savings when you file.

Other Protected Assets

-

Wages: Up to six months of wages deposited into a bank account may be protected under Florida's head of household wage exemption.

-

Personal property: Florida allows up to $1,000 in personal property, or up to an additional $4,000 if the homestead exemption is not used.

-

Life insurance and annuities: Cash value of life insurance policies and proceeds of annuity contracts are generally exempt under Florida law.

Your attorney will map every asset you own against Florida's exemption schedule before your case is filed. The goal is to protect as much as possible while still qualifying for the chapter that best fits your situation.

How Peck Law Firm Helps Florida Residents Start the Bankruptcy Process

Not every bankruptcy attorney takes the time to explain what is actually happening in your case. Peck Law Firm is built around a different approach: education first, then aggressive representation.

Attorneys Who Know Florida Bankruptcy Law

Attorney Richard K. Peck IV is admitted to the U.S. Bankruptcy Court for the Middle District of Florida and has handled consumer bankruptcy cases across the state.

Together, they handle Chapter 7 liquidation cases, Chapter 13 repayment plans, Chapter 11 reorganizations, foreclosure defense, credit card lawsuits, and FCCPA debt-collection harassment claims.

The firm is not a document mill. Every case gets attorney attention, not just paralegal processing.

Stopping Creditor Harassment in Its Tracks

If collectors are calling your home, your workplace, or even contacting family members, that behavior may violate the Florida Consumer Collection Practices Act. The firm handles FCCPA claims alongside bankruptcy work, meaning your debt-collection harassment problem and your underlying debt problem can be addressed together.

For a broader overview of your options, visit the firm's bankruptcy practice overview.

Frequently Asked Questions About Filing for Bankruptcy in Florida

How long does it take to file for bankruptcy in Florida?

Once your documents are gathered and reviewed, your attorney can typically file your Chapter 7 petition within a few days to two weeks. The full Chapter 7 process from filing to discharge takes approximately four to six months. A Chapter 13 case remains open for the three-to-five-year length of your repayment plan.

Will filing for bankruptcy stop wage garnishment immediately?

Yes. The automatic stay under 11 U.S.C. § 362 takes effect the moment your petition is filed with the court. Your employer must stop the garnishment once they are notified of the filing. Your attorney will notify relevant parties quickly to prevent further paycheck deductions.

Do I have to go to court when I file for bankruptcy?

In most consumer cases filed in the Middle District of Florida, you will not appear before a judge. The only required appearance is the 341 meeting of creditors, which is currently conducted by phone or video in most cases. Your attorney attends with you and handles the questions.

Will I lose my home if I file for bankruptcy?

Not necessarily, and in many cases, no. Florida's unlimited homestead exemption protects most primary residences. If you are behind on your mortgage, Chapter 13 allows you to catch up through a structured repayment plan while keeping your home. Chapter 7 can eliminate other debts and free up cash flow to stay current on your mortgage going forward.

How does bankruptcy affect my credit?

A Chapter 7 bankruptcy remains on your credit report for up to 10 years, and a Chapter 13 remains for up to 7 years. However, most people who file are already carrying late payments, charge-offs, and collection accounts that are damaging their credit in real time. Many clients begin rebuilding credit within one to two years of their discharge by using secured credit cards and keeping balances low. The discharge gives you a clean starting point that continued debt collection does not.

Take the First Step Toward a Financial Fresh Start

You do not have to figure this out alone, and you do not have to keep living with the daily stress of calls, lawsuits, and impossible balances. The law exists to give people exactly the kind of relief you are looking for, and a qualified Florida bankruptcy attorney can walk you through every step.

Peck Law Firm represents Florida residents facing overwhelming debt, creditor harassment, wage garnishment, and the threat of foreclosure. The attorneys are ready to review your situation, explain your options honestly, and file aggressively on your behalf when you decide to move forward.

This article is provided for informational and educational purposes only and does not constitute legal advice. Bankruptcy laws and outcomes vary depending on the facts and circumstances of each case. Reading this article does not create an attorney-client relationship with Peck Law Firm, P.A. Results and timelines may vary based on the facts of each case and applicable law.